All Categories

Featured

Table of Contents

But before pulling money out of a MYGA early, take into consideration that one of the major benefits of a MYGA is that they grow tax-deferred. Chris Magnussen, licensed insurance coverage representative at Annuity.org, clarifies what a fixed annuity is. A MYGA provides tax obligation deferment of passion that is compounded on an annual basis.

It's like investing in an IRA or 401(k) however without the contribution limits.

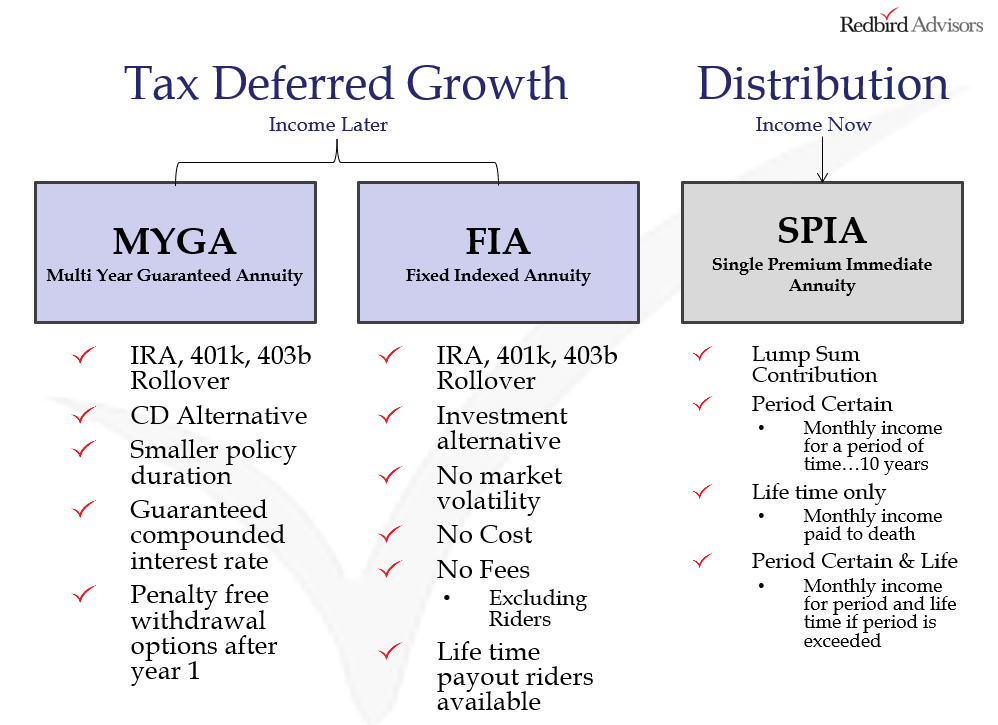

This tax advantage is not special to MYGAs. It exists with conventional set annuities also - accumulation phase annuity. MYGAs are a sort of taken care of annuity. The primary difference between conventional set annuities and MYGAs is the period of time that the contracts guarantee the fixed rates of interest. MYGAs guarantee the rate of interest for the entire period of the agreement, which could be, for instance, one decade.

So, you may get an annuity with a seven-year term however the price might be assured only for the initial 3 years. When individuals mention MYGAs, they generally liken them to CDs. Discover exactly how to secure your savings from market volatility. Both MYGAs and CDs offer guaranteed price of return and a guaranty on the principal.

Monthly Income From $100 000 Annuity

Compared to investments like supplies, CDs and MYGAs are more secure but the rate of return is lower. They do have their distinctions, nevertheless. A CD is released by a financial institution or a broker; a MYGA is an agreement with an insurance provider. A CD is FDIC-insured; a MYGA is not guaranteed by the federal government, but insurance provider must belong to their state's guaranty organization.

A CD may have a lower passion price than a MYGA; a MYGA may have much more fees than a CD. CD's may be made offered to lenders and liens, while annuities are safeguarded against them.

Given the conventional nature of MYGAs, they may be better suited for customers closer to retirement or those who choose not to be subjected to market volatility. can i sell my annuity. "I transform 62 this year and I truly want some type of a set rate rather than stressing over what the stock exchange's mosting likely to perform in the following 10 years," Annuity.org consumer Tracy Neill stated

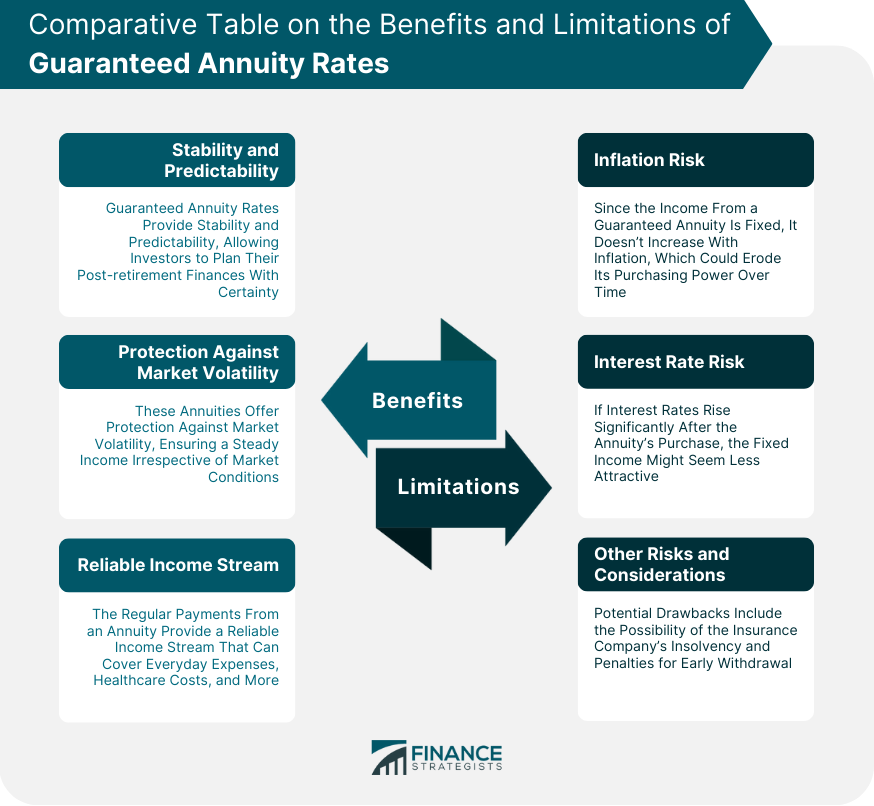

For those who are looking to surpass inflation, a MYGA could not be the finest monetary strategy to fulfill that objective. Other kinds of annuities have the possibility for higher benefit, however the threat is greater, also.

Much better comprehend the actions entailed in purchasing an annuity. They offer modest returns, they are a secure and reliable investment option.

Cancel Annuity

No-load Multi-Year Assured Annuities (MYGAs) on the RetireOne system deal RIAs and their clients defense against losses with an ensured, dealt with price of return. These services are interest-rate sensitive, yet might provide insurance functions, and tax-deferred development. They are favored by conventional investors looking for relatively foreseeable results.

3 The Squander Alternative is an optional feature that must be chosen at contract concern and topic to Internal Earnings Code restrictions. Not offered for a Certified Durability Annuity Agreement (QLAC). Your life time income settlements will certainly be lower with this option than they would certainly be without it. Not readily available in all states.

An annuity is a contract in which an insurance provider makes a series of income payments at normal periods in return for a costs or premiums you have actually paid. Annuities are commonly purchased for future retirement income. Just an annuity can pay a revenue that can be assured to last as long as you live.

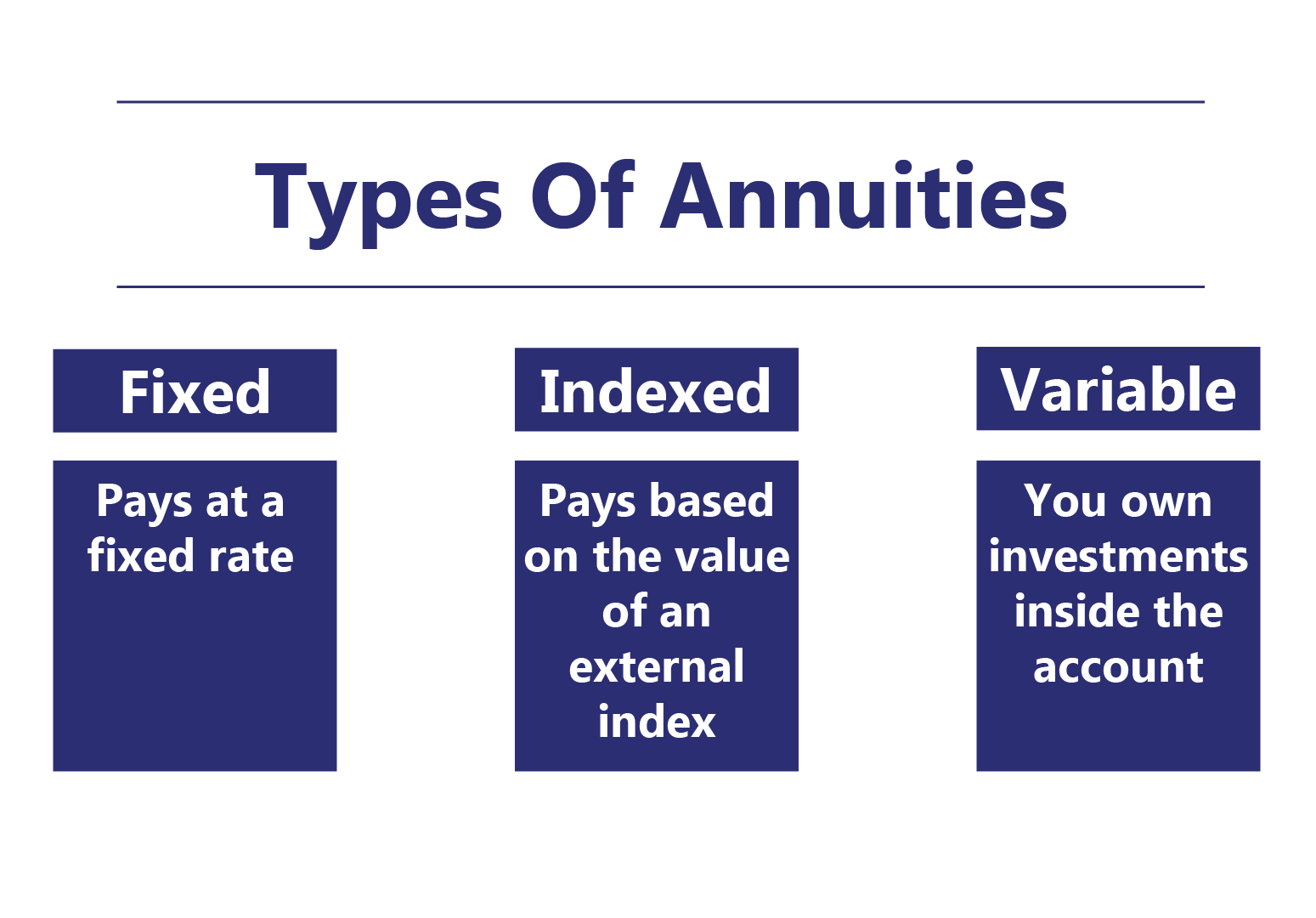

The most usual kinds of annuities are: solitary or several costs, immediate or postponed, and dealt with or variable. For a solitary costs agreement, you pay the insurer just one settlement, whereas you make a collection of repayments for a multiple costs (best 3 year myga rates). With an instant annuity, revenue settlements begin no behind one year after you pay the costs

The existing rate is the rate the business chooses to credit scores to your contract at a particular time. The minimum guaranteed rate of interest rate is the cheapest rate your annuity will certainly make.

Some annuity agreements apply different interest rates to each costs you pay or to premiums you pay throughout various time durations. 5 year immediate payout annuity. Various other annuity agreements might have 2 or even more gathered values that money different advantage options.

Single Premium Fixed Deferred Annuity

Under present federal regulation, annuities receive unique tax treatment. Revenue tax on annuities is deferred, which implies you are not tired on the rate of interest your money gains while it stays in the annuity.

A lot of states' tax legislations on annuities comply with the federal law. You must seek advice from a specialist tax consultant to review your individual tax obligation circumstance. Several states have laws that provide you an established variety of days to consider the annuity contract after you buy it. If you determine throughout that time that you do not want the annuity, you can return the agreement and get all your refund.

The "totally free look" duration need to be prominently mentioned in your contract. Make sure to review your contract meticulously during the "cost-free look" period. You ought to consider what your goals are for the money you take into any type of annuity. You need to think regarding how much danger you are willing to take with the money.

Terms and conditions of each annuity contract will differ. Contrast info for comparable contracts from several firms. If you have a particular inquiry or can not obtain responses you need from the representative or company, contact the Division.

The buyer is usually the annuitant and the person to whom periodic settlements are made. There are two standard kinds of annuity agreements: instant and postponed. A prompt annuity is an annuity contract in which settlements begin within 12 months of the day of acquisition. The immediate annuity is bought with a single premium and regular payments are usually equivalent and made regular monthly, quarterly, semi-annually or annually.

Periodic settlements are delayed till a maturity day mentioned in the contract or, if earlier, a day picked by the proprietor of the contract. One of the most typical Immediate Annuity Agreement settlement alternatives consist of: Insurance company makes routine repayments for the annuitant's life time. An option based upon the annuitant's survival is called a life contingent choice.

Pension Annuities Rates

There are 2 annuitants (called joint annuitants), normally partners and regular repayments proceed up until the death of both. The income repayment quantity might proceed at 100% when just one annuitant lives or be lowered (50%, 66.67%, 75%) throughout the life of the enduring annuitant. Routine repayments are created a specified period of time (e.g., 5, 10 or twenty years).

Earnings repayments cease at the end of the period. Settlements are normally payable in set dollar amounts, such as $100 per month, and do not give security against inflation. Some instant annuities give inflation security with regular increases based upon a fixed rate (3%) or an index such as the Customer Cost Index (CPI). An annuity with a CPI adjustment will begin with lower payments or call for a higher initial premium, yet it will supply at least partial security from the threat of rising cost of living.

Earnings repayments remain continuous if the financial investment performance (after all charges) equals the assumed financial investment return (AIR) specified in the contract - life insurance annuity payout. If the financial investment efficiency exceeds the AIR, payments will raise. If the investment performance is less than the AIR, repayments will lower. Immediate annuities generally do not allow partial withdrawals or offer money abandonment advantages.

Such persons need to look for insurance firms that use subpar underwriting and think about the annuitant's wellness condition in determining annuity revenue payments. Do you have sufficient funds to satisfy your income needs without buying an annuity? In other words, can you handle and take organized withdrawals from such resources, without concern of outliving your resources? If you are concerned with the threat of outlasting your funds, after that you might take into consideration purchasing an immediate annuity at the very least in an amount adequate to cover your standard living expenditures.

Can I Buy An Annuity

For some alternatives, your health and marriage condition might be taken into consideration. A straight life annuity will certainly offer a higher regular monthly revenue payment for a provided costs than life contingent annuity with a period specific or reimbursement function. Simply put, the expense of a specific earnings settlement (e.g., $100 monthly) will be greater for a life contingent annuity with a duration particular or reimbursement feature than for a straight life annuity.

As an example, an individual with a dependent spouse may desire to take into consideration a joint and survivor annuity. A person worried about receiving a minimal return on his/her annuity costs may wish to think about a life contingent alternative with a period certain or a reimbursement feature. A variable immediate annuity is often picked to equal inflation during your retired life years.

A paid-up deferred annuity, additionally generally described as a deferred revenue annuity (DIA), is an annuity contract in which each costs payment acquisitions a set buck income advantage that starts on a specified day, such as an individual's retired life day. The contracts do not preserve an account worth. The premium price for this item is a lot less than for a prompt annuity and it allows a person to keep control over the majority of his or her various other properties throughout retirement, while securing long life security.

Each premium payment acquired a stream of earnings. At a worker's retired life, the revenue streams were combined. The employer could make the most of the staff member's retirement advantage if the agreement did not offer for a survivor benefit or cash surrender advantage. Today, insurers are marketing a similar product, commonly described as durability insurance.

Best Type Of Annuity

Many contracts permit withdrawals below a defined level (e.g., 10% of the account value) on a yearly basis without abandonment cost. Cash abandonments may be subject to a six-month deferment. Build-up annuities generally offer a money payment in case of fatality prior to annuitization. In New York, survivor benefit are not treated as surrenders and, because of this, are exempt to surrender fees.

{kind=link}

Table of Contents

Latest Posts

Decoding Retirement Income Fixed Vs Variable Annuity Everything You Need to Know About Financial Strategies Breaking Down the Basics of Annuities Variable Vs Fixed Pros and Cons of Various Financial O

Highlighting the Key Features of Long-Term Investments A Closer Look at How Retirement Planning Works What Is Fixed Income Annuity Vs Variable Growth Annuity? Pros and Cons of Variable Annuity Vs Fixe

Decoding How Investment Plans Work Everything You Need to Know About Financial Strategies Breaking Down the Basics of Immediate Fixed Annuity Vs Variable Annuity Features of Smart Investment Choices W

More

Latest Posts